Life Insurance Collateral Assignment Process

A borrower will assign a portion or their insurance policy as collateral for a loan in the case of death, this doesn’t mean that you can use life insurance as traditional forms of collateral, it’s only a measure lenders take to protect themeslves against the potential death of the borrower. This means that part of the insurance proceeds are used to pay the loan principal and interest. In the event of the death of the borrower, part of the death benefit proceeds are used to pay off the loan balance while the remaining amount goes to their beneficiary. Also, collateral assignments are an important part of the life insurance for SBA loan process.

How to Apply For Collateral Assignment Life Insurance

When applying for a collateral assignment of life insurance, you can use two ways to do so: through the bank or through your insurer. The two are explained further below;

APPLYING THROUGH YOUR BANK

There are some lenders who will consider using your existing life insurance policy for collateral assignment if you request it, but others might require you to take out a brand new policy specific for that purpose.

In either case, using life insurance for collateral assignment when applying for loans is a fairly common practice that almost every life insurance company and the bank is equipped to handle.

You start off the application for assignment by securing the loan with the bank in question. This is where you will discover the limitations and regulations the bank has regarding the collateral assignment of life insurance. Each lender has different policies.

APPLYING THROUGH YOUR INSURER

Once you have found the right loan, you must fill out the collateral assignment form. Your insurer will be able to provide you with this form easily.

The form has to be filled out by every party involved, including yourself, the lender, and the insurance company. You can sign the forms at the time of your loan application or you can sign them after your policy has been issued.

If you are taking out a brand new life insurance policy, you are better off signing all of the documents for this at the beginning of the application. The time frame to request a collateral assignment and be accepted for it ranges between 24 hours and 48 hours.

Some banks might require that you notarize the form, which can add some time to the application and acceptance process

Here’s how the collateral assignment process works:

- You apply for a life insurance policy and name your beneficiary (your spouse, children, whomever). Just as you normally would.

- After the policy goes into force, a collateral assignment form from the life insurance company will be sent for you to complete.When a life insurance company sets a collateral assignment of life insurance, this usually takes in the region of seven to ten days to be filed and acknowledged, however we may expedite this if the collateral assignment is required more urgently. When taking out life insurance at the same time as assigning the collateral, the collateral assignment form must be submitted with the life insurance application.

- You get the collateral assignment form signed (some companies require a notarized signature).

- It take a few days to a few weeks for the life insurance company to acknowledge the assignment (we accelerate the process and know what companies do this quickly)

- Once the loan has been paid in full, the assignment must be lifted from the policy by means of a release form sent by the lender to the insurance company. When it receives the release, the insurance company cancels the assignment and restores all rights in the policy to the owner.

To clarify, a collateral assignment allows the life insurance company to pay your SBA lender only what they are owed and the rest goes to your beneficiary. As you pay down the loan, the amount of coverage will be more than you need and a collateral assignment form makes sure the lender is only paid what is needed.

If you named the lender as the beneficiary, the lender would receive the entire death benefit even though you’ve paid down the balance and if you did that, the life insurance company wouldn’t issue you the amount of coverage needed – they’ll typically only issue 80% of the loan amount. So it’s imperative that you use a collateral assignment.

Also, be careful with the life insurance company you choose. Not all life insurance companies have collateral assignments. We know which companies do and which companies don’t so you’re not wasting your time applying with a company who will ultimately not be able to satisfy the SBA’s requirement.

We’ve had a lot of business owners spend the time to purchase a life insurance policy only to ultimately not be able to collaterally assign the policy to the bank. Working with an agency experienced in life insurance for SBA loans is critical.

Once we secure a policy for you, our work doesn’t stop. It’s now time to get your collateral assignment notarized and recorded by your life insurance company’s legal department. We take care of this for you and help to expedite it. We know the faster you get this collateral assignment completed, the fast you get your money.

As you can tell, a life insurance agent who specializes in helping those applying for SBA loans will make the process a lot easier for you. We know the ins and outs and will communicate with your lender on time frame to keep everyone in the loop.

Absolute and Conditional Assignment

There are two types of assignment, which are absolute and conditional.

Absolute Assignment

With an absolute assignment, the lender usually has all the power to the insurance policy. By signing an absolute assignment, you give your lender the right to make changes to the policy and control everything including paying premiums. You still remain insured by the policy but put in mind that the assignee has the power to add or remove beneficiaries.

Conditional Assignment

As opposed to the absolute assignment where all rights to the policy are completely transferred to the assignee, a conditional assignment has restrictions. Control remains to the policy holder and only the specified proceeds will be paid to the lender/assignee. Upon completion of repayment of the loan, the assignment is lifted and total control is shifted back to the policy holder.

With an already existing life insurance policy, you will be able to meet the requirements specified by your lender. This is only possible if the death benefit proceeds are enough to pay off the loan amount. The borrower is responsible for ensuring that his/her insurer is informed and that they will accept the policy to be used as a collateral.

If you do your research well, you will find that a good number of life insurance companies stipulate stringent rules and requirements that should be met. These rules include informing them about any collateral assignment once it is made. Your insurer is supposed to forward a written notice notifying your collateral assignee about the filled assignment.

The lender also needs to ensure that everything is in check before allowing anything else to proceed. Some of the things that need to be checked include up to date premiums that have been made over a period of at least 6 months. In addition, there shouldn’t be another collateral assignment made with the life insurance policy.

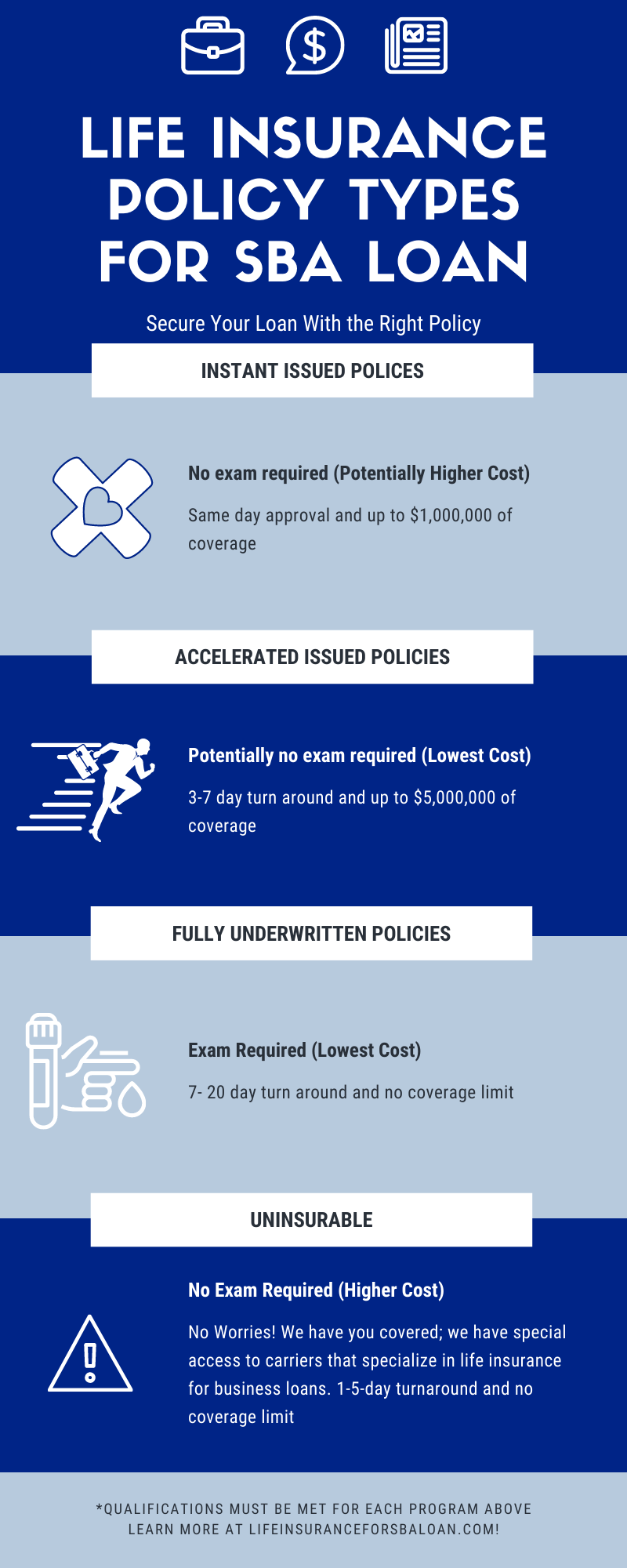

Here are some examples of insurance policies you can use for collateral assignment:

Term Insurance

Term life insurance is used to offer coverage for a specific number of years. The proceeds of the policy are only paid out after the insurer dies and it lacks equity and a surrender value. It falls under the category of the most affordable insurance plans which is why it is a top pick for most people.

You don’t need to buy a plan that exceeds or falls below your needs, term life insurance enables you to purchase a plan tailored to your needs and since it is not permanent, you are going to pay low premiums. For example, if you have 10 years left on a loan you borrowed from the bank, you can opt for a 10-year term life insurance plan.

Universal Life Insurance or Whole Life Insurance

With universal life insurance, you will be able to design the insurance policy according to how you want it. The insurance proceeds are usually released when the insured party dies. It is great for individuals looking for a permanent insurance policy that never expires unless you are dead. In short, you will continue to receive coverage as long as the annual premiums are getting paid.

On the downside, universal life insurance policies tend to be expensive because they are meant to offer life term coverage.

On the bright side, the policies build cash value and the longer the premiums are paid, then the more value the plan will build. This cash value can be used on other investments or to pay off the outstanding premiums.

Second To Die Insurance

Second to die insurance is meant to insure a husband and a wife. The beneficiary will not receive any proceeds until the first person dies. For instance, you can choose a second to die policy to if your spouse is dependent on you. This is to ensure that all the death benefit proceeds are transferred to her or him after you die and they are not left stranded.

With different types of insurance companies you will have different premiums available to you. Also, you will get different experts ready to help you in choosing the right policy with regards to your needs.

PROS AND CONS OF COLLATERAL ASSIGNMENTS

Pros

Collateral assignment safeguards the amount payable to the lender in that the lender gets the amount that was loaned out. This plays out well following the stipulations that are put in place, in the case of death to the borrower the lender will be paid in full and the remaining will be given the listed beneficiaries. There following are some of the benefits of a collateral assignment.

Protects the Lender’s Interests

Apart from a collateral assignment helping a borrower secure a loan, it also plays a big part in protecting the lender’s Interest. When the insurance company receives the collateral assignment form, it is responsible for protecting the interests of the lender. In some cases, the borrower will not be allowed to make any changes, withdraw the cash value component, or even use the policy as collateral for another loan. Restrictions are put on the borrower until the assignment is lifted.

Flexibility With Personal Property

When you use personal property as collateral for a loan, you may end up losing it to your lender to pay off the loan. There are two case scenarios that may occur if you list personal property as collateral for a loan. .

The first scenario is losing your property to the lender when you default the loan. The lender can claim your personal property as a means of paying off the loan balance.

The second scenario is facing serious implications for selling property listed as collateral for a loan.

To avoid such situations, borrowers use life insurance as collateral which gives them the flexibility to sell their personal property whenever they feel like.

Affordability

Another major advantage of using life insurance as your collateral is that it is an affordable way of paying back your loan. With some policies, you will only be required to pay small amounts of premiums for a large coverage. This is an advantage to a person who has used their insurance policy as collateral assignment.

Elegance

Having your life insurance policy as your collateral is an elegant way of paying back your loan. When you die, part of your death benefits are used to pay off the loan balance, but this is usually after you have stopped paying the policy premiums. Some people regard this as a stylish way of repaying their loans.

Cons

Collateral assignment has great benefits, but it also has a fair share of disadvantages which are discussed below;

Limited Death Benefit

It is advisable to assign part but not the whole of your death benefit as collateral. This helps prevent unpleasant situations like the lender claiming all the death benefits after you are gone. Alternatively, you can use a different insurance policy strictly for the collateral.

Effort to Get Insured

Getting an affordable insurance policy at low premiums is not easy. You either get one and miss out on the other one or even miss out on both of them. First, you need to undergo long medical examinations which constitute the underwritten process. On the other hand, it will take you weeks for your loan to be approved and this can be stressful if you needed the loan soon.

Loss of Policy Control

Not paying your policy premiums has its repercussions. In the long run, you may end up losing control for your policy since your lender can purchase a different policy for you. This results in added premiums on the principal amount of the loan.

Limited Use of Cash Value

You may not be able to use the cash value of your policy as you wish because it will put limitations to your insurance policy.

With oodles of agencies and insurers ready to cover you, it is getting easier every day to get a good life insurance policy.

Your lender will have different requirements that you will need to meet. As such, you can design your coverage to meet those needs as put below;

Coverage amount

You have the right to assign a specific amount of your coverage to your lender, instead of making the whole coverage available to them. Also, you can use your coverage amount and align it to your collateral needs.

Type of policy

A term life policy will usually cost less than a comparable amount of coverage in a whole life policy. If you need a smaller amount of coverage or have medical conditions that could limit your options, a no-exam policy may work. Be sure to get enough coverage to meet the bank’s collateral requirements.

Choosing a beneficiary

A rule you should never forget is that listing your lender as a beneficiary is a no-no! Such a mistake would cost you all your coverage even after completing the loan repayment. If your lender is listed as the beneficiary, they can claim all the remaining proceeds from your policy after you are gone.

Bottom Line

The process of setting up a collateral assignment does not have to be a nightmare. If you dread the whole process, then it is better to consult with a financial expert to guide you through. All in all, it may be unnecessary if you have an insurance policy in place and only need a collateral assignment. Since the process only entails filling up a few forms and waiting for a few days for approval, it is possible to do it on your own.